.png)

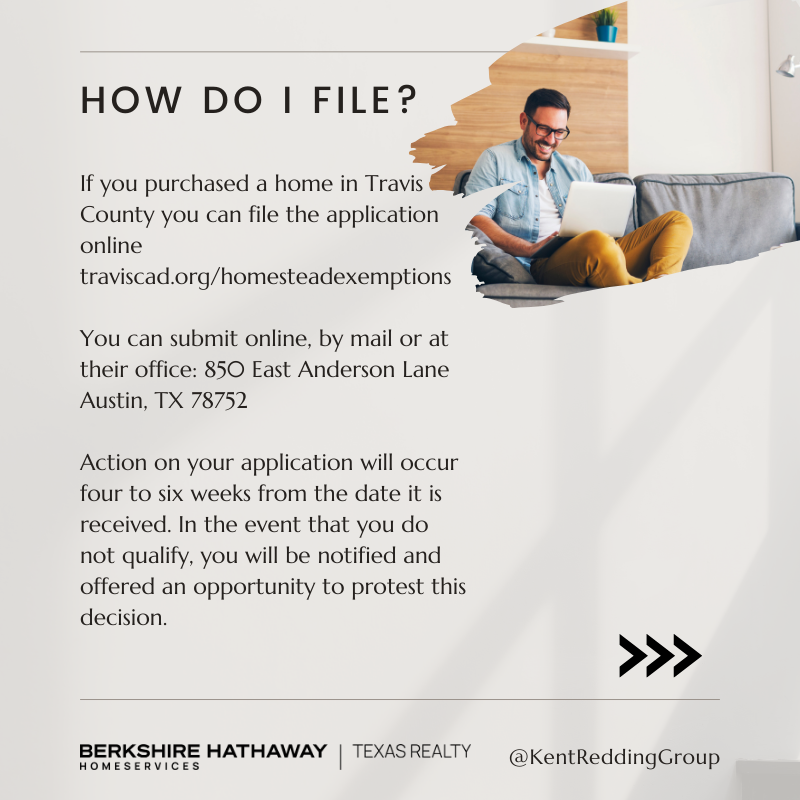

How to File Your Homestead Exemption

|

Travis County Homestead Exemption Form

Williamson County Homestead Exemption Form

Bastrop County Homestead Exemption Form

Caldwell County Homestead Exemption Form

Hays Bastrop County Homestead Exemption Form

Additional resources

Residence Homestead

Tax Code Section 11.13(b) requires school districts to provide a $40,000 exemption on a residence homestead and Tax Code Section 11.13(n) allows any taxing unit to adopt a local option residence homestead exemption of up to 20 percent of a property's appraised value. The local option exemption cannot be less than $5,000. Tax Code Section 11.13(a) requires counties that collect farm-to-market or flood control taxes to provide a $3,000 residence homestead exemption.

To qualify for the general residence homestead exemption an individual must have an ownership interest in the property and use the property as the individual's principal residence. An applicant is required to state that he or she does not claim an exemption on another residence homestead in or outside of Texas.

Inherited Residence Homestead

Heir property is property owned by one or more individuals, where at least one owner claims the property as a residence homestead, and the property was acquired by will, transfer on death deed, or intestacy. An heir property owner not specifically identified as the residence homestead owner on a deed or other recorded instrument in the county where the property is located must provide the appraisal district:

- an affidavit establishing an ownership interest in the property;

- a copy of the prior property owner's death certificate;

- a copy of the property's most recent utility bill; and

- a citation of any court record relating to the applicant's ownership of the property, if available.

Each heir property owner who occupies the property as a principal residence, other than the applicant, must provide an affidavit that authorizes the submission of the application.

An owner may record their interest in the heir property in the county where the property is located with the local county clerk. Applicants may find a list of individuals and organizations that may provide free or reduced-fee legal assistance with the State Bar of Texas at https://www.texasbar.com/.

Age 65 or Older or Disabled Persons

For persons age 65 or older or disabled, Tax Code Section 11.13(c) requires school districts to provide an additional $10,000 residence homestead exemption. Tax Code Section 11.13(d) allows any taxing unit to adopt a local option residence homestead exemption. This local option exemption cannot be less than $3,000.

To qualify for the age 65 or older residence homestead exemption, the individual must be age 65 or older, have an ownership interest in the property and live in the home as his or her principal residence. If the person age 65 or older dies, the surviving spouse may continue to receive the residence homestead exemption if the surviving spouse is age 55 or older at the time of death, has an ownership interest in the property and lives in the home as his or her primary residence. The surviving spouse may need to reapply for the exemption.

A disabled person must meet the definition of disabled for the purpose of receiving disability insurance benefits under the Federal Old-Age, Survivors and Disability Insurance Act.

An eligible disabled person age 65 or older may receive both exemptions in the same year, but not from the same taxing units. Contact the appraisal district for more information.

Disabled Veterans and Surviving Spouses of Disabled Veterans

Tax Code Section 11.22 provides a partial exemption for any property owned by a disabled veteran. The amount of the exemption varies depending on the disabled veteran's disability rating. The surviving spouse who remains unmarried and surviving children of a disabled veteran may also qualify for an exemption under this section.

Tax Code Section 11.132 provides a partial exemption for a residence homestead donated to a disabled veteran by a charitable organization which may also extend to the surviving spouse of the disabled veteran who has not remarried. The amount of the exemption is based on the disabled veteran's disability rating.

Tax Code Section 11.133 entitles a surviving spouse of a member of the U.S. armed services killed or fatally injured in the line of duty to a total property tax exemption on his or her residence homestead if the surviving spouse has not remarried since the death of the armed services member.

Tax Code Section 11.131 entitles a disabled veteran awarded 100 percent disability compensation due to a service-connected disability and a rating of 100 percent disabled or of individual unemployability to a total property tax exemption on the disabled veteran's residence homestead.

This exemption extends to a surviving spouse who was married to a disabled veteran who qualified or would have qualified for this exemption if it has been in effect at the time of the veteran's death provided:

- the surviving spouse has not remarried;

- the property was the residence homestead of the surviving spouse when the veteran died; and

- the property remains the residence homestead of the surviving spouse.

Surviving Spouses of First Responders Killed in the Line of Duty

Tax Code Section 11.134 entitles a surviving spouse of certain first responders killed or fatally injured in the line of duty to a total property tax exemption on his or her residence homestead if the surviving spouse has not remarried since the death of the first responder.

Additional Resources

- FAQ - Disabled Veterans ExemptionFAQ

- 100 Percent Disabled Veterans and Surviving Spouses ExemptionForm 50-135

- Application for Disabled Veteran's or Survivor's Exemption (PDF)Form 50-114

- Application for Residence Homestead Exemption (PDF)

Selling Your Home?

Get your home's value - our custom reports include accurate and up to date information.